Trends and Conditions in the Wide-Format Sector

Earlier this year, SGIA conducted its annual Industry Benchmarking Survey. The information here provides a brief preview of the survey findings, specifically as they relate to 201 companies serving the wide-format digital printing segment. SGIA’s full industry reports based on the results will be published by year’s end, and they will be available at SGIA.org.

Demographics

While a strong majority of companies serving the wide-format sector serve other businesses as well, the number of those that identify primarily as business-to-consumer is on the rise (23.4% in 2018 versus 14.8% in 2017). Geographic areas served by companies in this segment are local (65.3%), regional (58.7%) and national (58.2%), but nearly 25% serve international clients. Staffs are small, with the median number of employees at just 12, and the median sales revenue is $1,850,000.

Click to enlarge

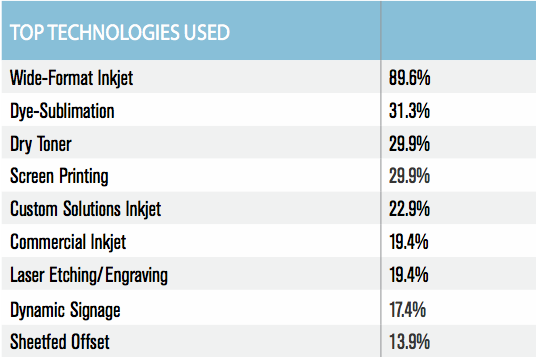

Technology Use

Companies are divided evenly between those that rely entirely on digital equipment (50.9%) and those that use it and other technologies as part of a multi-technological approach (49.0%). Almost all of the respondents have wide-format inkjet (89.6%) printers, and roughly one-third also use either dye sublimation (31.3%), screen printing (29.9%) or dry toner (29.9%) equipment. At least nine out of 10 companies (90.6%) offer finishing/post-production services.

The exchange of finishing services between printers happens more frequently on the production level, with 65.4% providing and 73.0% purchasing. At least half of respondents provide (52.8%) or purchase (55.3%) post-print services. This exchange of services allows companies to use production facilities more efficiently. Lamination (91.9%), installation (80.6%), grommeting (77.4%) and mounting (75.8%) continue to be the most frequently provided finishing services.

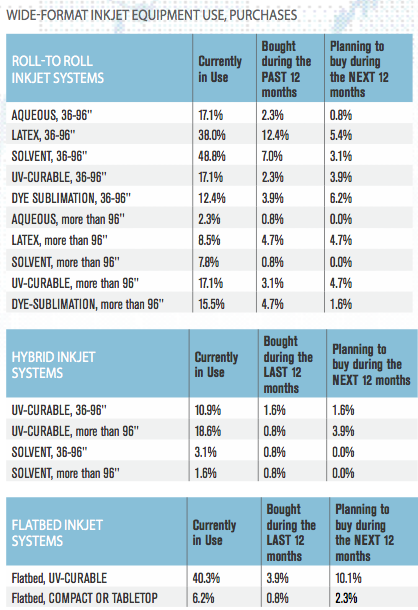

Equipment Use & Purchases

Click to enlarge

Among roll-to-roll inkjet systems, 36"- to 96"-wide systems with solvent (48.8%) or latex (38.0%) inks are used the most, with latex being the most frequently bought during the current year (12.4%) and one of the most desirable for the future (5.4%). Dye-sublimation (6.2%) and UV-curable roll-to-roll (more than 96") are also highly sought. Hybrid and flatbed inkjet systems also factor into current and future purchase plans.

The most frequently used finishing equipment is lamination/mounting (74.1%), cutting/trimming/routing/diecutting (72.7%) and grommeting (70.6%). Cutting equipment was also the most frequently bought during 2018 (13.3%) and the most desired for the future (11.9%).

Capital Investments

Two out of three printers spend either $5,000 to $49,999 (33.3%) or $50,000 to $499,999 (39.3%) annually on production-related equipment. About three-quarters of respondents (72.6%) plan to either make the same capital investment or increase it in the year ahead. Among the top contributing factors to investment decisions, the most popular are: the need to increase capacity, increased product demand, replacement needs, and new products or innovations in the production process. Customer support (51.3%), durability of equipment (54.4%), price to operate (46.8%) and range of capabilities (43.0%) are the most important factors influencing equipment purchasing decisions.

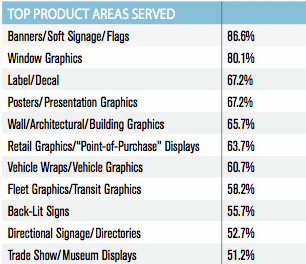

Markets and Products

The markets served by at least half of respondents are: corporate branding (65.2%), retail (61.7%), architecture (57.2%), nonprofit (56.7%), food services (54.7%), business-to-consumer (53.2%) and ad agencies (52.2%). The product areas served by at least half of respondents are also numerous, demonstrating high product diversity among companies serving the wide-format sector. They are listed below:

Click to enlarge

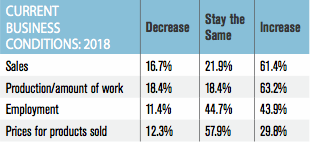

Business Conditions

More than half (51.6%) of companies view finding new customers as their primary barrier to growth, followed closely by downward pressure on prices. Recruiting and retraining sales and production personnel and the cost of adopting new technologies are additional barriers. Respondents indicated a need for more efficient, cost-effective production, undertaking strategies such as reducing operating costs and lean manufacturing/continuous improvement initiatives.

Click to enlarge

More than 70% (71.8%) of companies experienced positive sales growth during 2017, while 17.6% experienced negative growth. Companies are generally positive about this year’s business climate, as shown in the table below.

Dan Marx, Content Director for Wide-Format Impressions, holds extensive knowledge of the graphic communications industry, resulting from his more than three decades working closely with business owners, equipment and materials developers, and thought leaders.

Olga Dorokhina is a research coordinator for the Specialty Graphic Imaging Association (SGIA).

Canon, HP, Kyocera, and Ricoh Gear Up for the 13th Annual Inkjet Summit as Keynote Sponsors

Canon, HP, Kyocera, and Ricoh Gear Up for the 13th Annual Inkjet Summit as Keynote Sponsors

Catch Up on The Latest Equipment Releases

Catch Up on The Latest Equipment Releases

Wide-Format Weekly (3/6/25)

Wide-Format Weekly (3/6/25)

Navigating the Promotional Products Industry Succe

Navigating the Promotional Products Industry Succe

Innovation, Automation, and AI Take Center Stage at the 2025 Wide-Format Summit

Innovation, Automation, and AI Take Center Stage at the 2025 Wide-Format Summit

GPA Announces The Launch of The 2025 GPA Print & Design Contest

GPA Announces The Launch of The 2025 GPA Print & Design Contest