The Economic Impact of the Supply Chain Disruption and Inflation

The following article was originally published by Packaging Impressions. To read more of their content, subscribe to their newsletter, Packaging Impressions inBOX.

Since the Covid-19 pandemic, printers have been fighting an uphill battle when it comes to their supply chain and rising costs. As the first quarter 2022 State of the Industry Update showed, the unknown week to week and future availability for materials, substrates and consumables coupled with increasing costs has made a significant impact on the bottom-line for many and has been a major business concern for nearly all.

To better understand the current state of the supply chain and the economic outlook, the second quarter 2022 State of the Industry Update focused solely on measuring evolving supply chain dynamics, how printing companies are responding to them, and what can be done to prepare for an economic downturn. The nearly 300 participants include commercial printers, graphic and sign producers, apparel decorators, functional printers and package printers/converters. The findings, however, translate across all segments of the printing industry. No one segment is immune from current economic situation; the issues and solutions are shared results.

The second quarter 2020 State of the Industry Update, published by PRINTING United Alliance and NAPCO Research, concludes that supply chain conditions in the printing industry are getting worse, the costs of materials are continuing to rise, and many have seen a direct negative impact to their revenue. Economic indicators point strongly to a downturn in the economy that looks very close to a recession. The crisis, however, has not affected all equally and some, who attribute their success to strengths gained long before the crisis started, have experienced increases to their revenue.

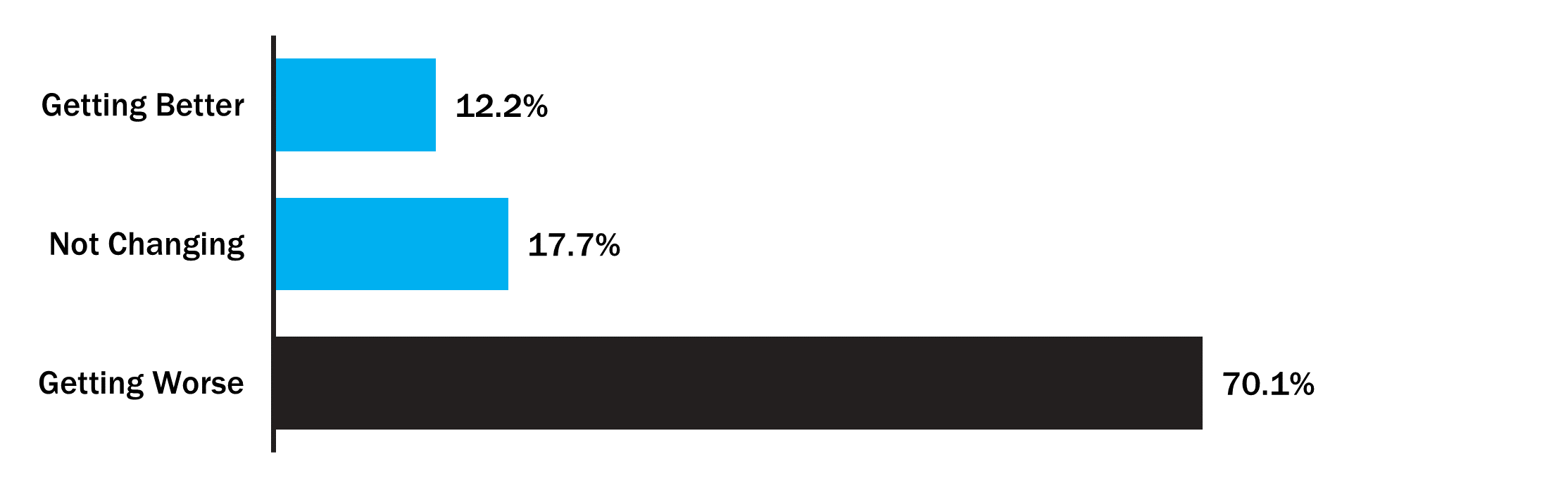

Material shortages and inability to acquire the materials needed topped the list of concerns in the first quarter 2022 State of the Industry Update, with 92.3% citing it as a significant concern. Three months later, the second quarter 2022 State of the Industry Update shows that companies are still experiencing significant challenges with sourcing supplies with the majority, 70.1%, saying the situation has gotten worse.

Figure 1: Supply Chain Conditions

Q. Overall, what’s happening to conditions in your supply chains? n=278

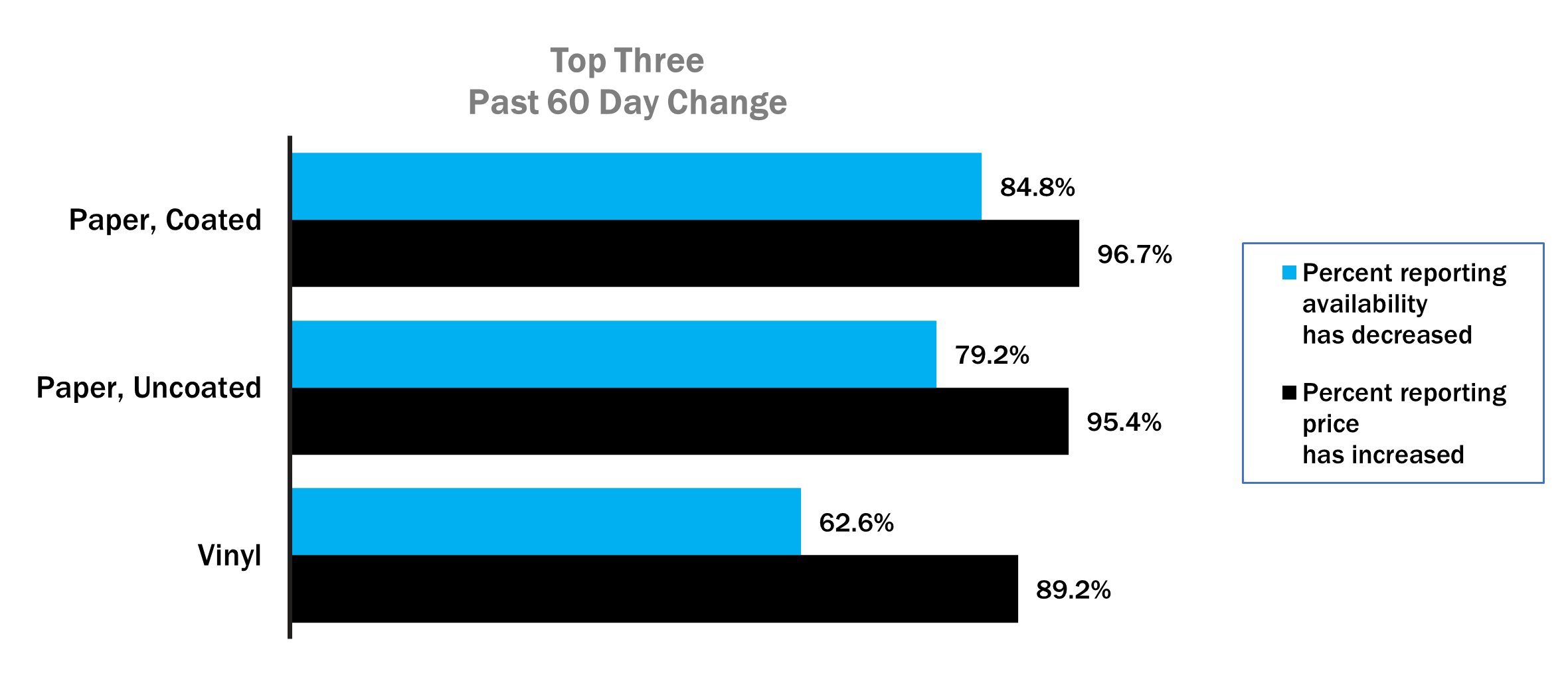

Substrate availability and costs are both serious issues for the printing industry. Companies were asked if they have seen substrate availability and prices increase, decrease, or stay the same over the last 60 days. Very few reported increased availability for ANY of the substrates measured and virtually none said prices were lower. For each substrate measured, at least 3 in 10 respondents said that availability over the past 60 days had decreased and over 7 in 10 respondents said that they were seeing cost increases. The top three substrates shown to have decreased availability and higher costs, coated and uncoated paper and vinyl, are shown below in figure 2.

To view the availability and price increase changes of the other substrates measured, download the Executive Summary here.

Figure 2: Substrate Availability and Prices

Q. For each substrate you purchase, how on average have availability and price changed over the last 60 days? n=295

According to respondents, consumable availability remains mostly unchanged over the past 60 days, however prices, similar to substrates, have increased and continue to be a concern. Like substrates, companies were asked if they have seen consumable availability and prices increase, decrease, or stay the same over the last 60 days. Very few reported increased availability for ANY of the consumables measured and none said prices were lower. For each consumable measured, at least 6 in 10 respondents said that availability over the past 60 days had decreased and over 5 in 10 respondents said that they were seeing cost increases. The top three consumables shown to have decreased availability and higher costs, coatings, plates and ink, are shown below in figure 3.

To view the availability and price increase changes of the other consumables measured, download the Executive Summary here.

Figure 3: Consumable Availability and Prices

Q.For each consumable you purchase, how on average have availability and price changed over the last 60 days? n=295

When companies can’t find the supplies to produce their goods, many areas of their business can be affected, and the result can often be a hit to the bottom line. The data in this study shows this to be true for many printing companies, nearly half say it has affected their revenue negatively.

Personal narrative is an important part of all PRINTING United Alliance State of the Industry Surveys allowing insight into real-life challenges and solutions from real-life companies experiencing many of the same pain points that you are experiencing. Respondents in the second quarter 2022 State of the Industry Update had a lot to say about how the fractured supply chain is disrupting their business. They spoke about how “every step of the supply chain is stressed, and one issue in one part (which could previously be absorbed) now causes major ripples and issues across the whole chain” and because of so many unknown backlogs “no matter how far out we plan, it is not far enough, and orders are not large enough” and if the economy shifts ”we are wondering if we will be overbought”. Their situations illuminate deeper and more far-reaching issues such as the worry of lost business because clients are no longer willing to accept pass-through cost increases, “they have seen enough,” one says, and there is valid worry that the disruptions and the costs will drive customers to seek our print alternatives and the fear expressed is that “once those monies are gone, they usually don’t come back”

Just as personal narratives can show what is not working, they can also illuminate what IS working for some. Over 2 in 10 respondents report that they have gained market share because of the supply chain crisis. What are they doing differently? We asked, and were rewarded with some very insightful information. Download the Executive summary here to learn more.

In each of the PRINTING United Alliance State of the Industry Surveys Chief Economist, Andy Paparrozi, provides an in-depth look at current economic indicators and provides an update on where the economy currently stands, where it is heading and what it means for the printing industry. Along with his insights, he provides quarterly growth projections for the printing industry. In the second quarter report, economic indicators are pointing to a slowing economy which could very well lead to a recession. Growth for the printing industry is also projected to slow, however will remain on the positive side. With the possibility of a recession looming, Papparozi gives steps a company can take to be proactive. As he explains, “they are not a secret sauce – we all know we should take them. The difference is that during a recession, ‘should take’ becomes ‘must take’ ” and the time to start thinking about it is now.

PRINTING United Alliance members can download the complete State of the Industry Update, Second Quarter 2022 and all other reports in the State of the Industry Series at https://www.printing.org/library/business-excellence/economics-forecasting/industry-reports/state-of-the-industry-series. Companies that are not currently members can download an Executive Summary at https://wideformatimpressions.tradepub.com/free/w_prin51/.

Jill Cantrell is a Research Analyst for the PRINTING United Alliance.